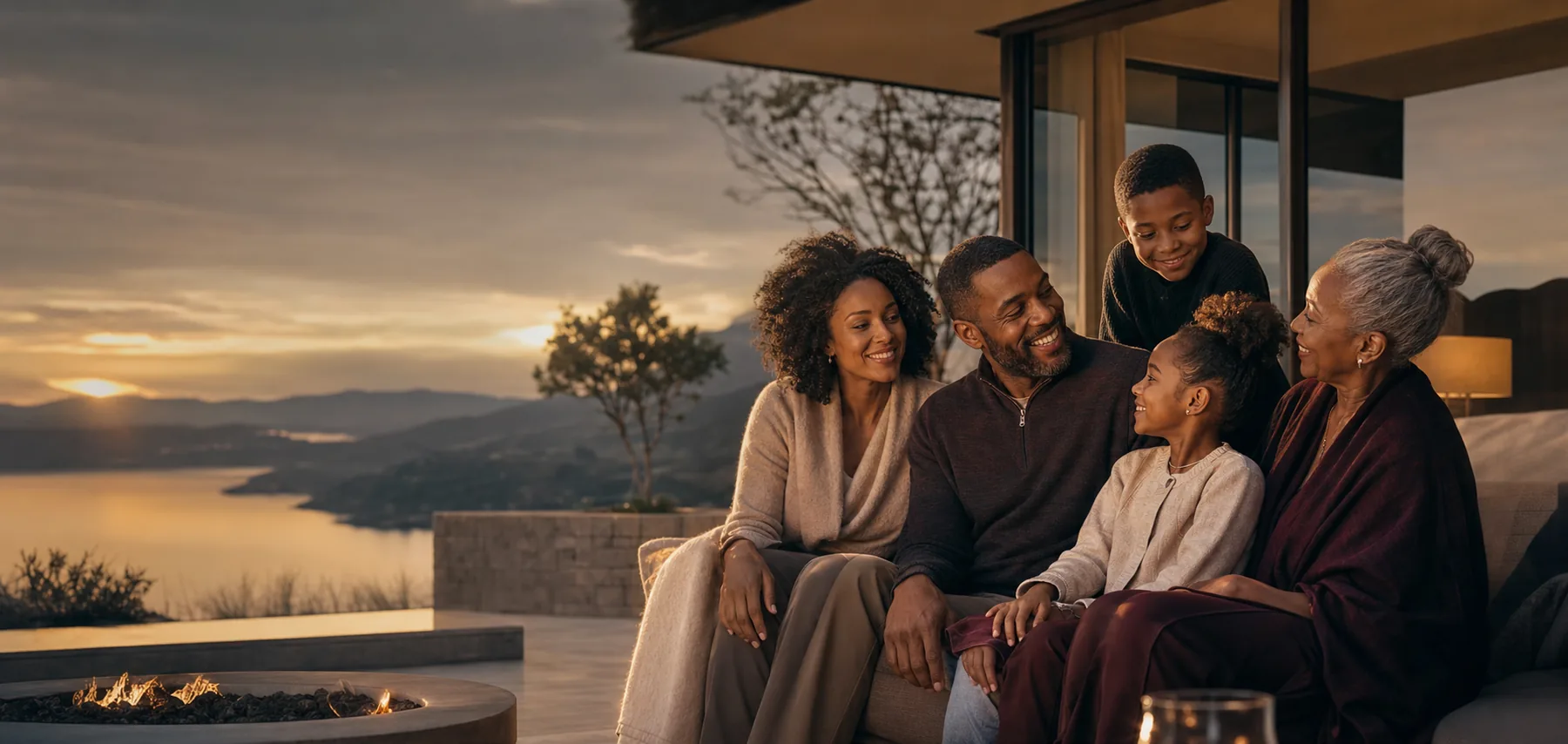

Family protection · legacy · wellness

Life insurance built around

the life you protect.

Life insurance can help replace income, protect a household from debt and preserve future choices. The right structure depends on the need, duration, budget and policy guarantees—not a one-size-fits-all product.

Talk with a licensed professional ↗A clear starting point

What does life insurance do?

Life insurance is a contract issued by an insurance company. In exchange for premiums and subject to the policy terms, the insurer pays a death benefit to named beneficiaries after the insured dies. It can support income replacement, debt protection, education funding, business needs and legacy goals.

01Choose the duration of the need

Start by identifying how long the financial obligation may last. Temporary needs may align with term coverage; lifelong or legacy goals may call for permanent coverage.

- Income replacement while children are dependent

- Mortgage and debt protection

- Final expenses and legacy planning

- Business continuation or key-person needs

02Compare guarantees and flexibility

A useful comparison separates guaranteed values from non-guaranteed assumptions and explains what happens if premiums, crediting or policy performance change.

- Premium schedule and coverage duration

- Death-benefit guarantees

- Cash-value access and policy loans

- Rider definitions, costs and eligibility

03Consider eligible wellness value

Certain John Hancock policies may include Vitality GO or offer Vitality PLUS. Eligible members can earn status and rewards through healthy activity and preventive choices. Participation, policy eligibility and current program terms control the available benefits.

Questions to ask

Understand the decision

before you act.

What is the difference between term and permanent life insurance?+

Term insurance is designed for a stated period and generally emphasizes cost-efficient death-benefit protection. Permanent insurance can remain in force for life if contract requirements are met and may build cash value, but it generally costs more.

How much life insurance should a family consider?+

The answer depends on income replacement, debts, education goals, final expenses, existing assets, employer coverage and the time dependents may need support. A licensed professional can model those needs rather than relying on a single rule of thumb.

Can life insurance include benefits while the insured is living?+

Some policies include or offer riders that may accelerate part of the death benefit after qualifying chronic, critical or terminal illness events. Definitions, costs and availability vary by carrier and state.

Veritas guidance

Clarity first.

Products second.

Discuss your goals, budget, time horizon and tradeoffs with an appropriately licensed professional.

Request guidance ↗